OT Equity Analysis | WIPT – A petroleum terminal, a tiny float, and a rally Jamaica is still trying to read

WIPT entered the market at fifty cents and briefly became one of the most valuable companies in the country. The rally outran the business. The business, on closer reading, is rather better than the rally made it look.

West Indies Petroleum Terminal Limited arrived on the Jamaica Stock Exchange on the 23rd of December last year with very little fanfare and a great deal of room for misreading. It came to market by way of introduction, which meant no new shares were sold, no money was raised, and no fresh stock entered public hands. All eleven point one eight billion ordinary shares were simply admitted to trading at fifty cents apiece, giving the company a starting market capitalisation of roughly five point five nine billion dollars. It was the final listing of the year, and on the day it looked like a modest one.

It did not stay modest. Within three weeks, the price had climbed past nine dollars, and by the middle of January, the stock had touched levels above twelve dollars, lifting the company past one hundred billion dollars in market value. At its peak, it had overtaken NCB Financial Group and sat behind only Massy, Sagicor and Scotia among the largest names on the exchange. A storage terminal at Port Esquivel, trading on the market for less than a month, had become one of the most valuable listed businesses in the country.

Nothing in the share price explained the move, because nothing in the business could carry it. For the year to December 2025, the company reported revenue of eight point eight three million United States dollars and net profit of two point two nine million. At its January peak, the market was valuing that profit stream at close to one billion United States dollars against shareholders’ equity of around twenty-nine million. A price-to-earnings multiple north of three hundred times does not describe a fuel terminal. It describes the absence of sellers. The price went one way, and the company, sound as it was, simply could not keep up with it.

What the numbers actually say

Set the share price aside, and the operating story is the more interesting one. WIPT is not a speculative shell that happened to list at the right moment. It is a profitable, asset-backed infrastructure business that spent 2025 quietly improving. Full-year net profit of two point two nine million United States dollars was more than double the one point zero four million earned in 2024. Revenue rose eight per cent to eight point eight three million, and the fourth quarter, which had been a loss of just over a million dollars in 2024, swung to a profit of around three hundred and fifty-eight thousand. Fourth quarter revenue jumped sixty-three per cent year on year. A business that was drifting in 2024 found its feet in 2025.

Part of that improvement was a one-off. The 2024 results had been weighed down by an impairment on a financial asset, and the near absence of that charge in 2025 flattered the comparison. But stripping it out does not erase the gains. The recovery rested on real operating progress, in particular a sharp rise in third-party storage income. Storage fees earned from customers outside the group climbed to roughly two point four million United States dollars, about forty-three per cent of total storage revenue, against six hundred thousand, or ten per cent, a year earlier. That is the single most important number in the accounts, and it has nothing to do with the share price.

The first quarter of 2026 confirmed the direction rather than the noise. Revenue rose twenty-three per cent to two point four nine million United States dollars, net profit climbed by more than half, and the margins told the real story. EBITDA reached one point eight million on a margin of seventy-two per cent, up from sixty-eight, and the net margin widened to forty per cent from thirty-two. These are the economics of a well-run toll road, not a commodity trader. The terminal earns fees for holding and moving other people’s fuel, the cost of doing so barely moves with volume, and so each additional barrel of throughput drops a large share straight to the bottom line.

The merits of the asset

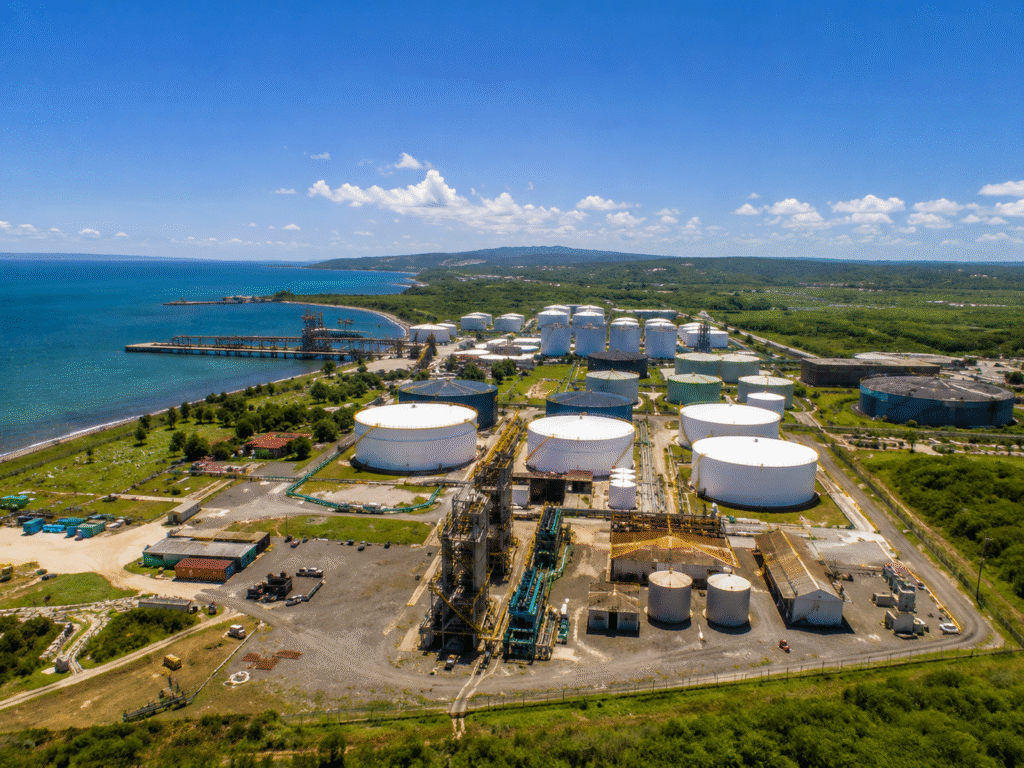

Underneath the earnings sits the reason the earnings behave this way. WIPT owns and operates storage capacity of more than seven hundred thousand barrels across its South Terminal at Port Esquivel in St Catherine and its facility at Ocho Rios, which together make it the second largest petroleum storage operation on the island. This is not a capacity that can be conjured quickly. Permitting, marine access, tankage and the safety infrastructure around fuel storage take years and serious capital to assemble, and the terminal at Port Esquivel was built up from a six-hundred-thousand-barrel ethanol facility acquired from Jamaica Broilers in 2016. That history is the moat. A competitor cannot simply decide to enter.

The asset also sits inside a vertically integrated group that gives it a captive base of demand. West Indies Petroleum, the parent, holds something close to thirty per cent of the Jamaican fuel market through its distribution and bunkering arms, and WIPT is the storage and logistics spine that those operations run on. That relationship guarantees a floor of throughput. The growth, tellingly, is coming from beyond it. Management has been explicit that the strategy is to fill the tanks with third-party volume, and the move from ten to forty-three per cent of storage revenue in a single year shows the strategy working. An infrastructure business that starts captive and is learning to sell its spare capacity to the open market is exactly the kind of business that compounds quietly.

None of this is without qualification. The balance sheet is modest, with total assets of about forty-two million United States dollars and equity near twenty-nine, some of it lifted by property revaluation rather than retained earnings. Cash is thin; the company ended 2025 with little more than a hundred thousand dollars on hand after paying down loans and leases, and a single large terminal carries concentration and operational risk that a diversified group does not. The third-party revenue that drove 2025 is also, by nature, contract-dependent and can soften, as the third quarter of 2025 briefly showed when throughput dipped. This is a good small business, not a fortress.

The mechanics of a thin float

The explanation sits in the structure of the listing rather than in the performance of the company. Because WIPT came to market by introduction, no shares were placed with the public to create a float. WIP Energy held close to eighty per cent of the company, World Energy Solutions held just under twenty, and the remainder was spread thinly across a small group that included an executive and the company’s roughly one hundred employees. There were one hundred and five shareholders in total at listing, and very few of them had any reason to sell.

What followed is a familiar problem dressed in unfamiliar numbers. When almost every share is held tightly and almost none trades, the handful of shares that do change hands set the price for the entire company. Daily turnover stayed below eleven thousand units, and some sessions saw transactions of as few as one to seven shares. A single buyer willing to pay up, met by a near total absence of sellers, can move a quoted valuation by tens of billions of dollars without anyone having formed a considered view of what the business is worth. The rally was a function of scarcity, not of conviction.

The governance questions it raised

The speed of the move drew attention from people who do not usually comment on individual stocks. Christopher Berry, chairman of Mayberry Group, raised the matter publicly, pointing to the size of the rally against the backdrop of a company that had not yet put a full set of 2025 results in front of the market. The exchange’s rules for a listing by introduction require recent financial statements, audited or unaudited and dated within ninety days of the application, and WIPT’s abridged statement was published in early December. But abridged disclosure ahead of a thinly floated debut is a thin foundation for price discovery, and the market noticed.

There was insider activity to read as well. Company disclosures showed that a director sold just over two million shares across several days in January, and a connected party sold a further million or so in the same window. Insider sales are not in themselves improper, and directors are entitled to realise value. But selling into a rally that the fundamentals do not support invites the obvious question of who was buying, at what price, and on the strength of what information. For a market that has spent years working to deepen its credibility, those are not comfortable questions to leave open.

What price discovery is supposed to do

The chairman, Charles Chambers, framed the listing as a way to create transparency and price discovery for a critical national asset, and to let Jamaicans participate in the ownership of infrastructure that serves the country. That is a reasonable ambition, and the terminal at Port Esquivel, with storage capacity above seven hundred thousand barrels, is a genuine piece of the island’s energy backbone. But price discovery requires a price that is being discovered by many participants trading meaningful volume against a shared understanding of the business. A quote set by a handful of shares is not discovery. It is an artefact of the listing method.

There is a tension at the heart of a listing by introduction that this episode has made plain. The method is cheap, fast and useful for putting a marker in the ground, and it spares a company the cost and dilution of an offer. But it does the one thing a public listing is meant to avoid, which is to hand the market a price before it has handed the market a float. Until enough stock is in circulation to absorb ordinary buying and selling, the quoted value tells you very little about the company and a great deal about how few shares are available.

Where it stands now

By the close of May, the stock was no longer behaving like a runaway. The extreme readings of January had faded, the more measured trackers were describing the price as relatively stable over the preceding quarter, and the one-year return, while still large, looked less like a vertical line and more like the aftermath of one. The company has an annual general meeting set for late June at its registered office in St Lucia, which will give shareholders their first formal occasion to engage management since the listing settled.

This leaves WIPT in an unusual position. The rally was an artefact of the listing method and told the market almost nothing about the company. But the company underneath it is genuinely worth attention. It is a profitable, growing, high-margin infrastructure business with a defensible asset, a captive demand base and a credible plan to sell its spare capacity to third parties, and it spent 2025 and the first quarter of 2026 doing exactly what it said it would. The lesson of the episode is not that the asset is hollow. It is that price and value came apart, violently and visibly, and that the gap was created by structure rather than by the business. When enough stock eventually circulates and the quote is set by many hands rather than a few, the market will get its first honest look at what WIPT is worth. On the evidence of the accounts, that figure will be a real one. It will also be a long way below a hundred billion dollars.

This commentary is provided for information purposes only and does not constitute investment advice or a recommendation to buy or sell any security. Readers should conduct their own analysis and consult a licensed financial advisor before making investment decisions.

Syndicated from Our Today · originally published .

Legal context · powered by Jurifi

Get the legal angle on this story. Pick a prompt and Jurifi's AI will explain it using Jamaican law.

AI replies are based on Jamaican law via Jurifi. Not legal advice.

Other coverage

First Rock plans APO to fund property acquisitions

Jamaica GleanerProductive Business Solutions Limited (PBS) Annual Report 2025

Jamaica Stock Exchange

Kingston Wharves looking to double business in two years

Jamaica Gleaner

Derrimon targets release of overdue accounts by month end to lift JSE suspension

Jamaica GleanerProductive Business Solutions Limited (PBS) Group Audited Financial Statements For The Year Ended December 31, 2025.

Jamaica Stock Exchange